We’re living through one of the fastest technology shifts humanity has ever seen. The meteoric rise of AI since ChatGPT’s launch in November 2022 has been both exciting and worrying.

AI hasn't just arrived – its boomed. And has been adopted by the public and businesses faster than almost any other technology we’ve created as a species.

To put this into perspective: the first computers appeared in the mid-1940s, but it took until the 1980s for businesses to adopt them in a widespread way.

AI has done that in less than three years.

A McKinsey global survey found that 88% of businesses are using AI in at least one business function. And almost 40% are using it across their entire organisation.

It's not just businesses either. AI is already baked into everyday life. A UK government study in 2024 found that 73% of people had used AI to fulfil day-to-day tasks. Think using voice assistants, predictive text, or asking ChatGPT what to cook with what's left in the fridge.

But before we delve into the risks of using AI as a business, it’s probably best to explore…

Why are businesses using AI?

To understand the risks of AI, we have to understand why so many businesses are using it.

It’s no surprise that larger companies are the first to adopt the new technology. They have the resources to experiment and find ways to utilise AI to improve their processes. Smaller businesses are slower on the uptake, but they're using it in some capacity.

So, what are the main reasons businesses are pursuing AI?

- Productivity – this is the big one. AI helps businesses do more without hiring more people. It can be used to automate simple tasks, draft emails, and summarise lengthy documents. For example, a project manager might use AI to record their meetings and write up notes for them, saving hours of time every week they can use elsewhere.

- Competitors – everyone else is doing it. In business, falling behind your competitors is a big no-no and an AI adoption arms race is underway. Especially at larger businesses who can’t afford to lose the edge over their rivals.

- Platform development – AI is evolving. Fast. From month to month, new agents, capabilities, and technologies are being released. Due to this, businesses are scrambling to find, review, and adopt new ways to use AI.

- People are using it – almost everyone is using AI in some capacity. Businesses recognise that their staff would be using it anyway, even if they didn’t instruct them to. This forces company leaders to legitimise and control the use of AI, rather than pretend it’s not happening.

What are AI risks in business?

Now that we understand why businesses are using AI, it’s important to understand the risks behind it.

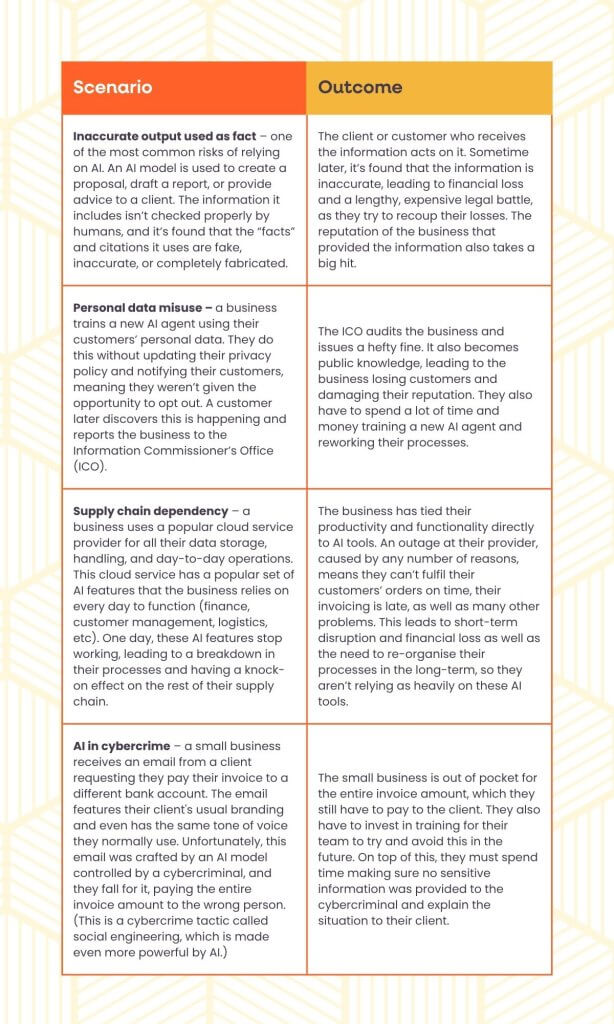

A quick caveat before we jump into specifics: each industry will have their own nuance when it comes to AI risks. A law firm’s risks might revolve around inaccurate information being generated by AI in court filings. While a HR consultancy’s risks might be more focused on the inputting of sensitive personal data into an AI model.

These scenarios are deliberately broad. Consider how they might apply to your industry and the way you work.

How insurance can help with AI-related risks

Those were some of the most common AI risks UK businesses will face. But depending on the industry you work in, you may face more.

Insurance can be a good way to mitigate these risks. Or at least reduce the impact if something goes wrong.

After reading them, you might be tempted to pop over to Google and type in “AI insurance”, right? Unfortunately, this isn’t really a thing.

Instead, most of these risks are covered by traditional business insurance policies.

However, it’s worth noting that the insurance industry is still adapting to the risks posed by AI. As such, it’s difficult to know how they’ll respond to claims involving it. It’s worth bearing this in mind when you’re buying.

Here’s how insurance might be able to help:

Professional indemnity insurance

Our first example was around providing inaccurate information to a client or customer, because you used AI to help you find it.

As such, your report, proposal, or advice was based on information that’s wrong. So, it leads to bad outcomes for your client.

In this case, you would probably be covered by your professional indemnity insurance. After all, it’s designed to cover you against claims your work caused financial loss for your clients. Or for when your clients accuse you of negligence – like using AI to draft a report for you without checking it properly.

So, you should be covered. However, always double-check your policy wording. Your insurer may include an exclusion for AI-related claims. If they do, it’s worth speaking to your broker at your next renewal to find a policy that’s better suited for you. And maybe double and triple checking those AI outputs in the meantime.

Business interruption insurance

If parts of your business, or your immediate supply chain, are reliant on AI processes to function, an outage can cause chaos for your ability to serve your customers.

Business interruption insurance covers you if you’re put out of action by something like a fire, flood, or pest infestation. Depending on the situation, it could cover you for AI-related interruptions too, but this would depend heavily on your policy wording.

If this is something you’re concerned about, speak to your broker. They can help you find cover that has the best chance of helping in the event of an AI outage.

Cyber insurance

Our examples on AI-powered cybercrime and personal data misuse would generally fall within a cyber insurance policy.

One of cyber insurance’s main areas of protection is against cyber-attacks, whether they’re AI-powered or not. Our example of a social engineering attack mixed with financial cybercrime would require an additional add-on, but it can be covered.

Our other example on personal data misuse in the training of an AI agent is a slightly trickier one. The part of this that could be covered by insurance would potentially be providing legal advice when dealing with the Information Commissioner's Office (ICO), as well as providing PR experts to help you manage the reputational damage the situation would cause. Almost all cyber insurance policies won’t cover ICO fines.

Once again, AI-related exclusions can exist in cyber policies, so read your policy wording carefully before buying.

How to manage AI risks in your business

AI is an immensely useful technology, which benefits UK businesses every day. However, it’s important to use it responsibly and carefully manage the amount of risk you take on.

Here are some simple and actionable ways to reduce your risk when using AI:

- Write an AI usage policy for you and your team – this doesn’t need to be a multi-page, all-encompassing document. However, it does need to include things like approved tools (so people aren’t using random AI sites for important work), guidance usage (like not uploading personal data or payment details), and instructions on how to properly double-check AI outputs before using them.

- This guide on AI policies and procedures from the ICO is well worth reading before you start.

- Train your staff – making sure your staff are trained on how to safely use AI will dramatically reduce your risk. Train them on your AI usage policy and why it’s important, as well as how to spot and avoid AI-supported social engineering and phishing cyber-attacks.

- Track what AI tools you use and who uses them – keep a register of what tools you use, who uses them, and why they’re used. Bonus points if you keep a note of how you review AI outputs. If you ever find yourself being audited by the ICO, this will be very handy.

- Prepare a basic AI incident response – planning for an AI incident scenario can make it a lot easier if something happens. Think about things like what to do if sensitive data is entered into an AI tool, a supplier notifies you of a breach, or an employee uses AI incorrectly.

Using AI responsibly

We’re moving towards a world where AI usage will become unavoidable for businesses, if they want to stay competitive.

But rushing ahead without considering the risks associated with AI can lead to a lot of harmful outcomes, not only for businesses but the customers and clients they serve.

Even with all the preparation in the world, though, AI incidents can happen. That’s where having the right insurance in place is crucial.

Want to find out whether your insurance covers AI risks? Or looking for insurance that will? Give us a call on 0345 222 5391 to speak to one of our insurance experts.

Images used under licence from iStock.

AIbusiness advicecyber insurancecyber liability insuranceinsurance explainedmanaging risk