One of the most common questions we’re asked is: 'How much does professional indemnity insurance cost?'

The words ‘piece of string’ and ‘how long’ leap to mind here.

It's a tricky one to answer quickly because there are no hard and fast rules. How much you pay depends on a lot of things.

But really, professional indemnity (PI) insurance is just like any other insurance. The price reflects the risk.

Do I need professional indemnity insurance?

If you’re not too sure what professional indemnity insurance is all about, here’s a brief explanation…

Professional indemnity insurance is there to back you up if you’re accused of negligence. If you make a mistake or someone says you haven’t done your job properly, and it’s cost them money, you could be faced with a claim.

So, if you offer any kind of service, PI insurance should be part of your business protection plan. The cost of professional indemnity insurance is always going to be less than the price you’ll pay if you’re faced with defending a claim alone.

How your PI costs are calculated

To work out the cost of your professional indemnity insurance, insurers will put together a risk profile for your business.

They’ll do this by asking you a series of questions, which builds a picture of how you operate. And ultimately, how at-risk you are.

So what’s ‘high risk’? Or ‘low risk’? How do you know if that’s you? Why does it make a difference to what you pay? And what can you do about it?

Here’s a breakdown of all the different things insurers factor in when they’re building your profile…

Things that affect your professional indemnity insurance cost

If you’ve bought PI insurance, public liability insurance, or employers’ liability insurance before, it's likely you’ll have answered some questions about your business.

Although it might seem a bit tedious, insurers need to know as much as possible so they can work out how much your professional indemnity insurance should cost.

To do that they consider:

Your annual turnover and fees

Generally, the higher this figure, the more your PI insurance costs. It’s an indication of the value and volume of business you do.

It’s simple numbers really: the more work you do, the greater the chance of a claim. And the greater the chance of a claim, the more insurers charge.

Contract values

High-value contracts mean high settlement figures if things go wrong. Professional indemnity insurers consider both your contract fee and the value of the contract as a whole.

Let's say you charge £3,500 to work on a contract worth £50m. If there’s a possibility (however slim) your negligence could scupper that entire contract, you'll pay more to reflect the risk of being sued not only for your part of the project but for the whole £50m.

What you do

The industry you’re in, the advice you give, the companies you work with, and the service you offer all make a difference to the cost of your professional indemnity insurance.

Some professionals have a fundamental, higher exposure to risk than others. This could be because, historically, claims are common or because the potential financial consequences of a claim make insurers nervous.

For example, premiums for a training consultant (low risk) start at a much lower level than those for a structural engineer (high risk). That's because training consultants are less likely to be sued for negligence in the first place and, if they are, the value of the claim will be much lower.

Either way, the insurer is looking at a safer bet with the training consultant and will, therefore, charge them less.

The level of cover

The easiest one to fathom. Fairly obviously, £5m worth of cover costs more than £50,000 cover. That's because in the first instance, a claim could leave the insurer facing a bill for £millions rather than £thousands. They’ll charge you more to make sure they can cover the amount, and to reflect the extra exposure.

You

As in, the person or people behind the business. Are you a 'professional professional'? Do you have relevant experience and qualifications? Do you have signed terms and conditions with every contract? How is your business structured? What risk management do you do?

Insurers are by no means moral guardians, but they do have an interest in who – as well as what – they're insuring.

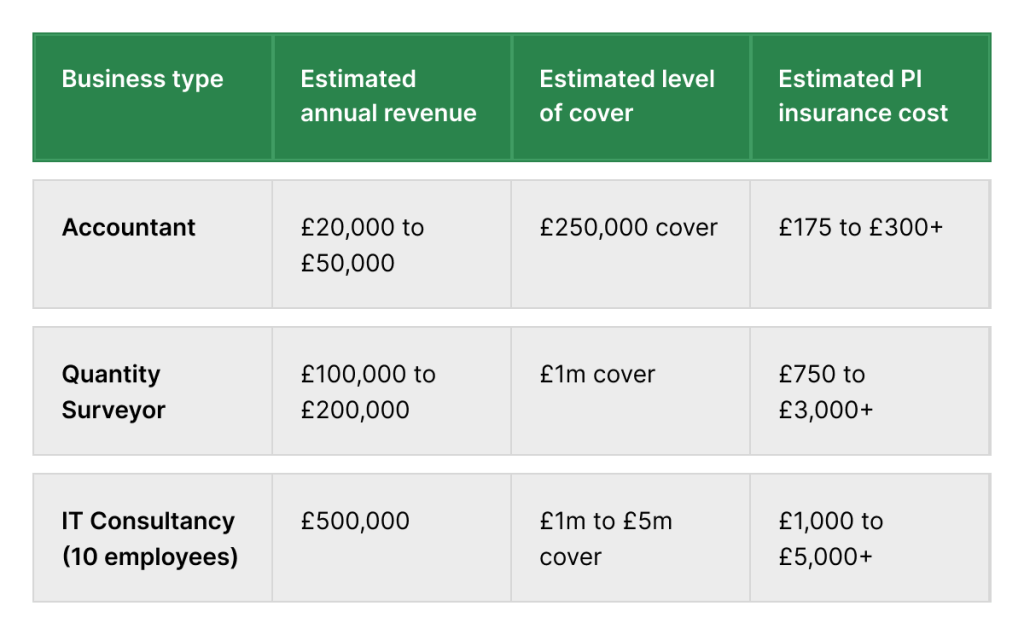

Professional indemnity cost examples

To illustrate, here are some examples of professional indemnity insurance costs for three very different types of businesses. Obviously, this is just a guide, so even if you do something similar, your actual quotes may vary.

Importantly, though, it demonstrates how the different factors come into play: how much you earn, what you do, and how much cover you need.

For example, a freelance accountant working alone is likely to have fewer, less high-profile clients, and a lower income. Whereas an IT consultancy with several staff members and a high turnover will likely have more clients. As the cost of all claims will likely be much greater for an IT consultancy, the risk is considered higher.

Remember. You can influence the cost of your professional indemnity insurance too...

These things - what you do, who you do it for, and how much for - individually and collectively, make a difference. They have a bearing on an insurer’s view of what and who they’re insuring, and how much to charge.

Bear in mind that insurers are a cautious bunch and they like a bit of handholding. Anything that makes them more comfortable with a risk is a good thing.

If you can, always demonstrate your competence and show them that you’re doing your bit to avoid claims wherever possible.

You'll find it benefits you as much as them and could even influence how much your professional indemnity insurance costs.

It’s also a good idea to compare professional indemnity insurance policies and make sure that whatever you buy covers you for all eventualities. Just going for the cheapest policy could cost you big time in the long run.

If you want to get a quick idea of how much your professional indemnity insurance could cost, you can get a quote. Or ring the team on 0345 222 5391.

Image used under license from iStock.

insurance costsinsurance explainedprofessional indemnity insurance